“You can make all the excuses you want, but if you are not mentally tough, and you’re not prepared to play every night, you’re not going to win. “ ~ Larry Bird

“You can make all the excuses you want, but if you are not mentally tough, and you’re not prepared to play every night, you’re not going to win. “ ~ Larry Bird

“You can make all the excuses you want, but if you are not mentally tough, and you’re not prepared to play every night, you’re not going to win. “ ~ Larry Bird

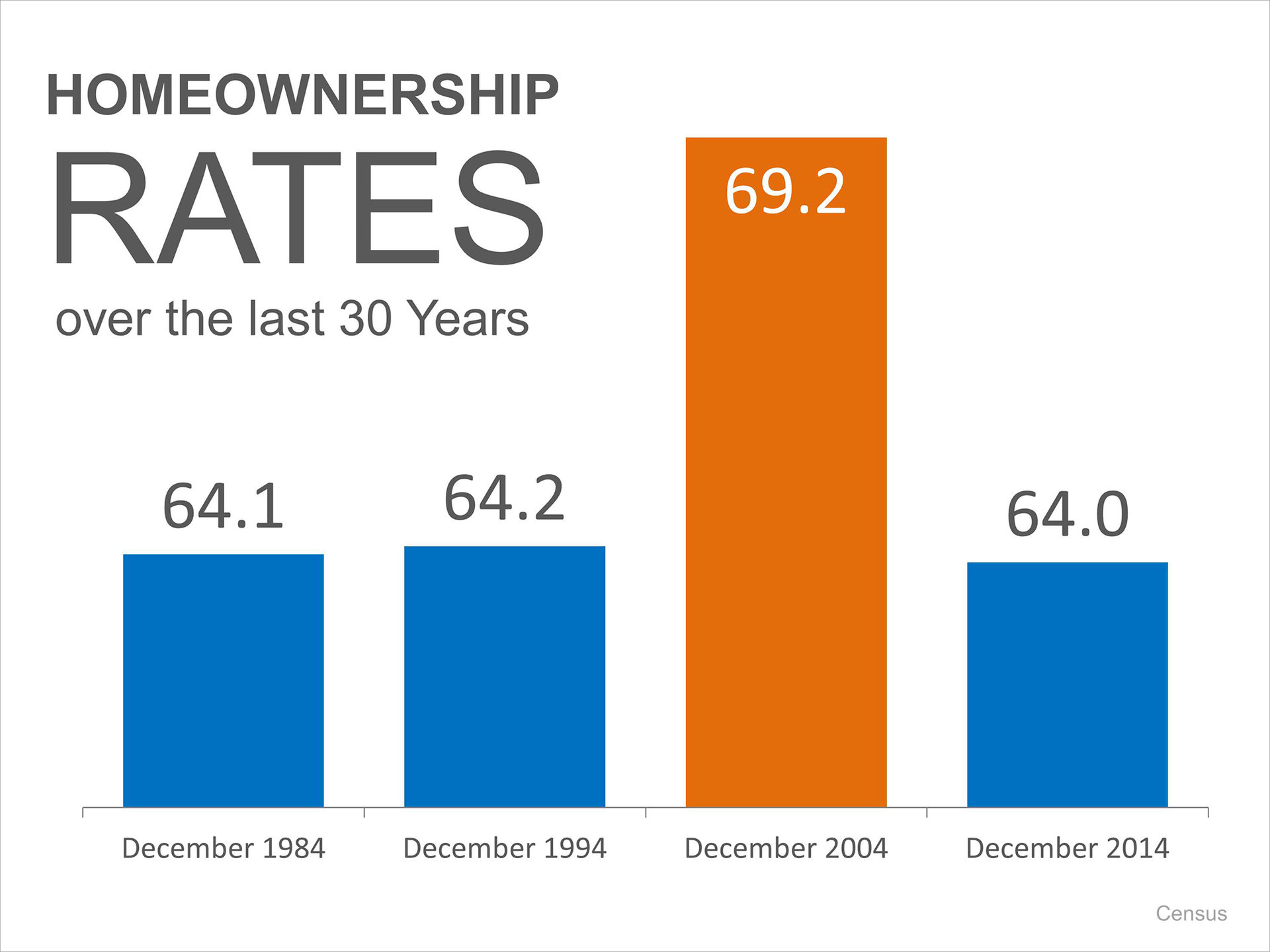

The Census recently released their 2014 Home ownership Statistics, and many began to worry that Americans have taken a step back from the notion of home ownership.

The national homeownership rate peaked in 2004, representing a 69.2% of Americans who bought vs. rented their primary residence. Many have noticed a decline in rates since then and taken that as a bad sign.

However, if you look at the national rate over the last 30 years (1984-2014), you can see that the current homeownership rate has returned closer to the historic norm. 2014 ended the year with a rate of 64% just under the rate in 1985 and 1995.

With interest rates and prices still below where experts predict, evaluate your ability to purchase a home with a local real estate professional.

“The idea is to make decisions and act on them — to decide what is important to accomplish, to decide how something can best be accomplished, to find time to work at it and to get it done.” ~ Karen Kakascik

There has never been a better time to purchase a home than this year. Prices are still down as are interest rates. There are still foreclosures and short sales on the market that will be a great buy for those willing to put a little sweat equity into their home. Read the equity report by clicking on the link below then take a look at the why buy now.

There has never been a better time to purchase a home than this year. Prices are still down as are interest rates. There are still foreclosures and short sales on the market that will be a great buy for those willing to put a little sweat equity into their home. Read the equity report by clicking on the link below then take a look at the why buy now.

Equity Report Why Buy Now?

“Success is not final, failure is not fatal: it is the courage to continue that counts.” ~ Winston Churchill

Consider before you ignore or outright refuse a very low purchase offer for your home. A counter offer and negotiation could turn that low purchase offer into a sale.

You just received a purchase offer from someone who wants to buy your home. You’re excited and relieved, until you realize the purchase offer is much lower than your asking price. How should you respond? Set aside your emotions, focus on the facts, and prepare a counter offer that keeps the buyers involved in the deal.

Check your emotions.

A purchase offer, even a very low one, means someone wants to purchase your home. Unless the offer is laughably low, it deserves a cordial response, whether that’s a counter offer or an outright rejection. Remain calm and discuss with your real estate agent the many ways you can respond to a lowball purchase offer.

Counter the purchase offer.

Unless you’ve received multiple purchase offers, the best response is to counter the low offer with a price and terms you’re willing to accept. Some buyers make a low offer because they think that’s customary, they’re afraid they’ll overpay, or they want to test your limits.

A counter offer signals that you’re willing to negotiate. One strategy for your counter offer is to lower your price, but remove any concessions such as seller assistance with closing costs, or features such as kitchen appliances that you’d like to take with you.

Consider the terms.

Price is paramount for most buyers and sellers, but it’s not the only deal point. A low purchase offer might make sense if the contingencies are reasonable, the closing date meets your needs, and the buyer is pre-approved for a mortgage. Consider what terms you might change in a counteroffer to make the deal work.

Review your comps.

Ask your REALTOR® whether any homes that are comparable to yours (known as “comps”) have been sold or put on the market since your home was listed for sale. If those new comps are at lower prices, you might have to lower your price to match them if you want to sell.

Consider the buyer’s comps.

Buyers sometimes attach comps to a low offer to try to convince the seller to accept a lower purchase offer. Take a look at those comps. Are the homes similar to yours? If so, your asking price might be unrealistic. If not, you might want to include in your counter-offer information about those homes and your own comps that justify your asking price.

If the buyers don’t include comps to justify their low purchase offer, have your real estate agent ask the buyers’ agent for those comps.

Get the agents together.

If the purchase offer is too low to counter, but you don’t have a better option, ask your real estate agent to call the buyer’s agent and try to narrow the price gap so that a counter-offer would make sense. Also, ask your real estate agent whether the buyer (or buyer’s agent) has a reputation for lowball purchase offers. If that’s the case, you might feel freer to reject the offer.

Don’t signal desperation.

Buyers are sensitive to signs that a seller may be receptive to a low purchase offer. If your home is vacant or your home’s listing describes you as a “motivated” seller, you’re signaling you’re open to a low offer.

If you can remedy the situation, maybe by renting furniture or asking your agent not to mention in your home listing that you’re motivated, the next purchase offer you get might be more to your liking.

By: Marcie Geffner

Marcie Geffner is a freelance reporter who has been writing about real estate, home ownership and mortgages for 20 years. She owns a ranch-style house built in 1941 and updated in the 1990s, in Los Angeles.

This gallery contains 24 photos.

For more information or for information on how you can purchase this exquisite retreat, email Jocelyne at alachuarealtor@gmail.com

“Formal education will make you a living; self-education will make you a fortune.” – Jim Rohn

Ready to List With A Real Estate Agent?

Do you understand the process of selling your home — all the “little” details? Before you list with an agent, educate yourself about all the possible things you could face. Be as informed as possible, so you can make the absolute best business decision. After all, the sale of your home is a business decision.

Most of us are not tuned in to the trends and fluctuations of the real estate market. Additionally, we are not aware of the steps necessary to maximize profits from the sale of your home. Typically, you rely heavily on an agent to lead you down the most profitable path. Well, when you consider your home is probably your largest financial asset, doesn’t it make sense to list with someone who will maximize your profits? But how do you find that agent?

This report is designed to empower you with critical information necessary to evaluate an agent’s qualifications and help you identify the professional top producer. The more involved you become, the better chance you have of choosing the right agent and consequently, the higher your profits will be!

Start by doing some research. Who are the most active agents in your market? Look at advertising to see how professional it is, ask friends and family, drive around the neighborhood looking for yard signs, then compile a list of agents.

1. The Phone Interview – Place a call to each of the agents on your list. Document how quickly they returned your call; keep in mind, they will be returning calls to your prospective home buyers. Do an initial ‘feel-out’ interview over the phone so when you meet, you will both be prepared.

2. Request a Complete Plan – From title to escrow, request a complete plan of all the services they will provide you when you list with them.

3. Evaluate Their Team – Top producers will have established relationships with lenders, title reps, inspectors, etc. These professionals are there for your benefit. If they are ill-prepared to handle all the steps of your transaction, look elsewhere!

4. Alternative Report – Request a complete report of alternatives to the home sale. What would current market leases generate? Rentals? Responsibilities attached with leasing? Have your agent educate you about all your options.

5. Insist on Pre-Qualification – Don’t waste valuable time negotiating or showing your property to unqualified prospects. Insist that your agent pre-qualify candidates to screen out all unwanted prospects.

6. A Net Sheet – See in writing a complete net sheet, minus commissions and fees, showing your exact proceeds at the time of sale.

7. A Marketing Plan – This is the heart of your agent’s overall strategy. Require a step-by-step plan with innovative new ways to attract home buyers.

8. Telemarketing Efforts – Investigate the agent’s telemarketing team. Do they just cold call? Or do they have a strategy to create proactive leads and call on those prospects.

9. Direct Mail – Investigate the agent’s capacity to send direct mail. How often do prospects receive mail? Is it professional? Does the mail piece motivate prospects to pick up the phone and call?

10. Advertising – Is it well written and professional? How many ad venues do they utilize? They should be advertising to as many on-line , community or local newspaper, and yard signs. Remember, the quality of the advertising will directly influence how well your home will be perceived.

11. Negotiation Strategy – Have a written, well-conceived, negotiation strategy. The old adage “You don’t get what you deserve, you get what you negotiate,” rings very true in real estate. Insist on a sound negotiation strategy before you entertain buyers.

12. Closing Strategy – Be sure to get a written closing checklist. You need to know in detail how you will conclude the sale of your home. This should provide a step-by-step procedure that will be easy to understand and follow.

My hope with this report has been to educate you and help you avoid the pitfalls many home sellers go through. I hope you found the ideas valuable and if there is every any way I can be of service to you or anyone you care about, please contact my office. Your initial consultation is always free and you are under no obligation of any kind. I’d love to hear from you!

This is a great home for the price. The neighborhood is excellent and the lot is one of the larger lots in the area. All in all, this little brick gem is a great deal! I sold this home to the owners originally, and now it is time for them to move on. So here I am selling the home once again. It is adorable and whoever buys this home will be very happy in it as my sellers are. To view more pictures of this home click on the link below.

“A bank is a place that will lend you money if you can prove that you don’t need it.” – Bob Hope

Re-printed from Trulia

January 3, 2012|Tools & Trends|No Comments

Jed Kolko, Trulia’s Chief Economist

5 events that rocked housing in 2011; by Jed Kolko

Government, lending changes, and forces of nature all shook the housing market in 2011. They had both an immediate impact and slow-burning effects. They set the stage for a bumpy 2012 with more foreclosures, political battles and local market risks – which will affect the industry and how agents do business.

1) Robo-Signing Reverberations

The “robo-signing” scandal – where banks were accused of approving foreclosures with incomplete or incorrect documentation – exploded in October 2010, but where are we now? Banks want a settlement in order to avoid costly, drawn-out lawsuits. One is shaping up that could reduce loan balances or interest rates for current homeowners, give payments to people who lost their homes and establish new mortgage servicing standards for the future.

Even if you think there’s money coming to you because you lost your home, don’t start spending against your settlement windfall just yet. One estimate from the Wall Street Journal is for a settlement of $25 billion if all states participate. Another report from TIME says that will translate into $1,500-$2,000 for households who were mistreated in the foreclosure process. A couple thousand dollars will give people some breathing room, but it won’t change anyone’s financial lives. And, be patient: it could be months before a deal is reached, an administrator is in place and the details are finalized.

Until that’s all figured out, here’s the immediate drama: who’s in and who’s out? Some states might hold out for a better deal or decide to sue these mortgage servicers directly, as Massachusetts has. California was the first and most vocal state to back out, and New York, Delaware, and Nevada have spoken out, too.

What Really Mattered: The threat of robo-signing lawsuits made banks gun-shy about pursuing foreclosures in 2011, which left many homes stuck in the foreclosure process. But once a settlement is reached, we’ll see a rush of foreclosures in 2012.

What It Means for Agents: More foreclosures will hurt prices and consumer confidence. Short sales could be harder to get approved if the foreclosure process gets easier.

2) The Debt Ceiling and the Budget Deficit

The federal government is running a deficit — it is spending more than it collects in taxes and other revenue – so it borrows to cover the gap by issuing debt. When there’s a deficit, we add to the pile of debt. To shrink this pile, the government needs to collect more than it spends (or, if you prefer, spend less than it collects) and use the surplus to reduce the debt.

In August, the government played a game of chicken over whether to raise the debt ceiling – which is really just a formality acknowledging that the deficit requires issuing debt to keep the government going. However, the right way to deal with the debt is to reduce the deficit – not by fighting over the debt ceiling.

Long before the debt ceiling debate and Standard & Poor’s federal credit-rating downgrade, we all knew that the federal budget was in bad shape. The debt ceiling debate rattled the markets and consumer confidence temporarily but interest rates stayed low. The important effect was that Congress created a bipartisan supercommittee to tackle the deficit – but it couldn’t reach agreement by its November deadline.

What Really Mattered: The deficit-reduction supercommittee teased us with some policy proposals that will surely rear their heads again. One idea that both Republicans and Democrats didn’t totally disagree about was reducing the mortgage interest and other tax deductions. If and when that happens, high-income homeowners with mortgages would pay a lot more in taxes.

What It Means for Agents: Scaling back the mortgage interest deduction would lower the offers buyers – especially high-income buyers – will make on homes. And some buyers will drop out of the market if the deduction, which favors homeownership, shrinks or vanishes.

3) The Expansion of HARP

In October, the Federal Housing Finance Agency (FHFA) said seriously underwater homeowners will be able to refinance through the Home Affordable Refinance Program (HARP). Originally, refinancing under HARP required a loan-to-value of less than 125% — that is, you couldn’t be more than 25% underwater – but that rule goes away for fixed-rate mortgages. But there’s a catch! Loans must be guaranteed by Fannie Mae or Freddie Mac, and – more importantly – borrowers must be current on their payments and must not have missed a payment in the last 6 months.

What Really Mattered: Some seriously underwater borrowers who fell behind on their payments in hopes of negotiating a loan modification are now kicking themselves because those missed payments make them ineligible to refinance. But those who can and do refinance will have lower monthly payments and extra money to spend — which will help stimulate the economy.

What It Means for Agents: Even if easier refinancing may not affect the home-purchase market directly, it will stimulate the economy a bit, which will raise housing demand and give buyers more confidence.

4) Natural Disasters Cause Insurance Disaster?

In 2011, several tornadoes, floodings and a hurricane temporarily halted what little construction there was to begin with, but this was just a short-term slowdown. The bigger long-term effect was the near-collapse of the federal government’s National Flood Insurance Program (NFIP). Still struggling financially under debt amassed after Hurricane Katrina, the NFIP’s insurance premiums don’t fully cover insurance claims when disaster strikes. August’s Hurricane Irene and its flood damage returned this problem to center-stage.

What Really Mattered: In flood-prone areas, you can’t get a mortgage if you don’t have flood insurance. Without NFIP, housing markets in these areas would skid to a stop. Could the program actually expire? It could, but as part of last week’s payroll tax agreement, the program got a last-minute extension until May 2012. No doubt, the political fight over this program’s long-term future will continue in into next year.

What It Means for Agents: Those working in flood-prone areas should be aware of private-sector flood insurance options for buyers in case the federal program lapses after May. And agents in these areas should follow the debate over NFIP on websites and blogs that cover the insurance industry.

5) Lowering the Conforming Loan Limit

Starting in October, the government lowered the upper limit for loans backed by Fannie Mae or Freddie Mac or insured by the Federal Housing Administration (FHA) from $729,750 to $625,500. Why? Government agencies now back or insure most loans, but it’s time to make the housing market less dependent on the feds. Lowering loan limits is one step in that direction; however, the real estate industry has urged the government to push the loan limits back up. And you know what? They scored a half-win in November, raising the loan limit back up for FHA loans but not for Fannie and Freddie.

What Really Mattered: Mortgage lenders are willing to charge lower rates for loans that are backed by Fannie or Freddie; with a lower conforming loan limit, a small number of loans that used to qualify for federal backing no longer do. As a result, homes that are now on the wrong side of the conforming loan limit will see fewer potential buyers and lower sales prices. This will matter more in California, New York, and other high-cost areas.

What It Means for Agents: Agents need to know the local loan limits, which may be different for FHA insurance and Fannie/Freddie backing. Homes for which loans will be above the new limits might see less buyer interest and price reductions.

According to Wikipedia, Xeriscaping “refers to landscaping and gardening in ways that reduce or eliminate the need for supplemental water from irrigation. It is promoted in regions that do not have easily accessible, plentiful, or reliable supplies of fresh water, and is gaining acceptance in other areas as climate patterns shift.”

Xeri, comes from the Greek “xeros,” meaning dry, and “scape,” is a kind of view or scene. When you put the two words together you have a landscape with slow-growing, drought-tolerant plants to conserve water and establish a waste-efficient landscape. Xeriscaping will also reduce the high cost of your water bills and comes in very handy during the drought periods we sometimes have in Florida.

For an in-depth explanation with lots of suggestions for choosing plants please click on the following link – xeriscaping. This link will bring you to the IFAS website, which looks like a newsletter. There is a plethora of helpful information other than gardening and landscaping. For example, you can find helpful information on energy, water conservation, waste management, wildlife, natural history, food and other local information.

There is a home on NW 8th Avenue in Gainesville that makes use of one aspect of xeriscaping. All the plants have been strategically planted so that the water runoff on the property goes to these plants. It is truly a zero maintenance yard in spite of the variety of plants growing there.This home sits next to Rattlesnake creek and boasts a magnificent variety of trees such as:

If having all this fruit isn’t enough, the home itself is an architects’ delight with 2 story soaring windows in the family room, an updated kitchen, a mother-in-law suite, a loft overlooking the pool area and a free form salt water pool.

There is a ravine along the back portion of the property, where rattlesnake creek runs, which has a cross-country trail system running through it. This ravine sustains the life of, and breeding habits of, 60 of the 65 varieties of dragon flies found in Florida.

This home has over 3000 square feet of heated and cooled living space and is located only 8 blocks from the University of Florida in Gainesville. This is not only a great home, but you can purchase it at the great price of only $219,000.00. This is a pre-approved short sale and the home will not last long on the market. For more information about this great home, please click on the following link: MLS# 329532.

Regarding the slide show below, the smaller pictures are of the home cleaned up when someone who cared about the property was living there. The larger pictures are of the home in its current condition. It can very easily be restored to the way it used to look – all it needs is some elbow grease and trimming of the yard. If you would like to take a tour of this property, please call for an appointment at the numbers below.

Jocelyne Grandjean-Brown

CDPE Trained

RE/MAX Professionals

Gainesville, FL 32606

Office: 352-375-1002

Cell: 352-870-9929

“A budget tells us what we can’t afford, but it doesn’t keep us from buying it.” – William Feather

When it comes to selling you home, everyone has a different perspective on what the price should be. This is a big problem, especially for Realtors who have studied the market and different subdivisions, and are knowledgeable on the value of a home. Sometimes there is a wide difference of opinion in pricing the home to sell, between the Realtor and the seller. I have also found the lender, appraiser and tax assessor also have their opinions. Following is a pictorial description of the discrepancy of these opinions. I hope this helps eliminate any confusion current sellers may have.

YOUR HOME AS VIEWED BY….

YOURSELF, THE SELLER

YOUR LENDER

YOUR BUYER

YOUR APPRAISER

YOUR TAX ASSESSOR….

“For most folks, no news is good news; for the press, good news is not news.” – Gloria Borger

You hear the bad news everywhere you turn. It’s on the television, the Internet, the radio and in print headlines. A lot of negative coverage has been devoted to today’s housing market. What you don’t hear is the good news about the real estate market and the many reasons why the current real estate market may be beneficial to you.

Bad news sells newspapers and gets high television ratings; therefore, the media has no reason to report the upside of today’s real estate market to the average American. This is where I come in. For example, did you know that approximately 30 percent of homeowners own their home free and clear?

The current market also affords some great opportunities for those looking to purchase a home. First-time homeowners, move-up buyers and investors can all benefit from low home prices, and historically low-interest rates, making now a great time to lock in a long-term mortgage. Also, the large selection of homes and low sales prices make it a great buyer’s market. And did you know that if you buy in a rural area –Alachua, High Springs and Newberry qualify as rural areas – you may qualify for a USDA loan, which is a 100% loan – a “no money down” loan.

Ultimately, though, these favorable conditions will go away. As inflation rises, so do interest rates. If you are looking to become a homeowner, you need to strike while the iron is hot!

“Believe that life is worth living and your belief will help create the fact.” – William James

First of all, a short sale is not short! For the general public, that is a misnomer, but for a bank that is an accurate statement. You see, a short sale falls short of what is owed. For example: in 2005 you purchased a lovely 4 bedroom, 3 bath home on 10 acres for $425,000.00. Suddenly this year you lost your job and decided it was best to unload the home and go back and live with mom and dad. You hired an appraiser – good move on your part to do that up front – and couldn’t believe what you read when you saw the appraiser’s report. “It’s worth how much now?” Say it isn’t so. There isn’t enough equity in the home to do anything with and your thinking -“How am I supposed to come up with over $125,000.00 to give to the bank, just so I can sell?”.

You can negotiate you loan and try to get the payments lowered or you can try to sell for as much as you can and hope the bank will not hold you responsible for the deficiency. Lot’s of luck! Nowadays most banks want everything they can get and they will bleed you dry. Have you seen all the new banks going up around town. Not just little structures but Big, MONUMENTAL, BUILDINGS.

I often wonder if all the money they make goes back into building these large structures.

Anyway, some banks are trying to help the homeowners – a little late, but I guess it’s better late than never. These banks are giving incentives to the homeowner to sell. The banks are not just asking anyone to sell, they are contacting people who are in imminent danger of losing their home to foreclosure. These incentives are:

Pretty sweet deal, if I do say so myself. This is a great deal not just for the seller, but also for the buyer because the prices are very competitive. I have 4 of these short sales myself. The only catch is they go on the market for 120 days and if they don’t sell in that amount of time they get foreclosed on.

So, if you know anyone looking for a great deal on a well-kept home in Gainesville, FL, please contact me utilizing the “Contact me” sheet on the tab above.